Are you looking for a bank loan or business angel to fund your business growth plans?

Do you understand the kind of things they look for in a company before they will invest?

Do you know what government finance is (still) available and how you qualify?

These are big issues. Succeed or fail issues. Don't leave it to chance - talk to us.

As a first step, get yourself on this business advice seminar or take a look at our business advice website.

Wednesday, 29 December 2010

Wednesday, 22 December 2010

Selling your business in the next two years?

Preparing in the right way could get you 2-3 times as much for your business.

Getting your company fit for sale could mean the difference between getting nothing and getting a great multiple.

It's what you as a business owner should spend your time doing.

Make a start. Come to this business advice seminar.

More information on our business advice website

Getting your company fit for sale could mean the difference between getting nothing and getting a great multiple.

It's what you as a business owner should spend your time doing.

Make a start. Come to this business advice seminar.

More information on our business advice website

Wednesday, 15 December 2010

Business owner - need to raise your game?

· Reached the point where you are no longer confident about the way to to drive your business forward?

· Need money from an investor or bank to fund your growth plans but unsure how to go about it?

· Started to wonder if you or your management team need to understand more about business to achieve your goals?

· Worried about how you will achieve the best price when you sell your business?

Even successful and ambitious business owners sometimes find it hard to remember why they started their business. Dealing with day-to-day issues can swamp the big picture, leaving you struggling to keep on track and unsure about when and how you will realise the rewards for all the hard work you put in.

We can help you raise yoru game to overcome these barriers - and we're running this great seminar to explain how.

More good business advice on our website.

· Need money from an investor or bank to fund your growth plans but unsure how to go about it?

· Started to wonder if you or your management team need to understand more about business to achieve your goals?

· Worried about how you will achieve the best price when you sell your business?

Even successful and ambitious business owners sometimes find it hard to remember why they started their business. Dealing with day-to-day issues can swamp the big picture, leaving you struggling to keep on track and unsure about when and how you will realise the rewards for all the hard work you put in.

We can help you raise yoru game to overcome these barriers - and we're running this great seminar to explain how.

More good business advice on our website.

Friday, 10 December 2010

Do you have a clear direction?

Clear direction - a vision, mission and strategic objectives - is essential for any successful business. Business owners ned to know:

· The importance of a motivating and guiding vision for any business and how to construct one

· Ways to turn your Vision into a compelling Mission for your staff and customers

· How to identify and set concrete Objectives that will keep you on track towards your goal whatever happens

· Why growth is not optional - and why unplanned growth will damage your business – and why growth itself brings challenges

· What successful business owners spend their time doing – and not doing

If you'd like to learn how to do this then this seminar is a must: The Road To Growth

More information on my website: http://www.nickbettes.co.uk/

· The importance of a motivating and guiding vision for any business and how to construct one

· Ways to turn your Vision into a compelling Mission for your staff and customers

· How to identify and set concrete Objectives that will keep you on track towards your goal whatever happens

· Why growth is not optional - and why unplanned growth will damage your business – and why growth itself brings challenges

· What successful business owners spend their time doing – and not doing

If you'd like to learn how to do this then this seminar is a must: The Road To Growth

More information on my website: http://www.nickbettes.co.uk/

Monday, 29 November 2010

Are you serious?

Yet another dicsussion on LinkedIn over whether businesses should have to grow or not (see the NRG-Networks group)

It's simple. There are two different types of business owner. Those who think it's their job to produce widgets (or build websites, or fit boilers, or sell insurance...) and those who think it's their job to build a business.

The first type are really just self-employed. The second type are the true business owners. They are focused on driving their business forward. They spend time thinking about how they get to the next step. They invest in their company and themselves so that they can achieve that next step - because they know that it will take a bigger strategy, a better plan, a tighter operation and more teamwork.

These business owners will spend time planning for when they come to sell their business. Or maybe they're wondering about getting money from a venture capitalist, business angel, government agency or bank to fund growth plans. They recognise when they reach the point where they and their management team become the limitation on the company's growth and they need to step back and change the way the busines operates. Success in any of these scenarios requires them to raise their game.

If you're one of the second type (true business owners) then you recognise the value of getting expert help. You will probably want to click here for your free copy of the white paper "Raising Your Game" which addresses the challenges you'll face.

It's simple. There are two different types of business owner. Those who think it's their job to produce widgets (or build websites, or fit boilers, or sell insurance...) and those who think it's their job to build a business.

The first type are really just self-employed. The second type are the true business owners. They are focused on driving their business forward. They spend time thinking about how they get to the next step. They invest in their company and themselves so that they can achieve that next step - because they know that it will take a bigger strategy, a better plan, a tighter operation and more teamwork.

These business owners will spend time planning for when they come to sell their business. Or maybe they're wondering about getting money from a venture capitalist, business angel, government agency or bank to fund growth plans. They recognise when they reach the point where they and their management team become the limitation on the company's growth and they need to step back and change the way the busines operates. Success in any of these scenarios requires them to raise their game.

If you're one of the second type (true business owners) then you recognise the value of getting expert help. You will probably want to click here for your free copy of the white paper "Raising Your Game" which addresses the challenges you'll face.

Thursday, 11 November 2010

Use IT Effectively To Boost Business Performance

How do you apply IT to boost business performance?

1. Set clear business direction as a prerequisite for the effective use of IT. This of course applies to the effective use of all parts of a business - marketing or operations or HR - but you'd be surprised at the number of companies, small and large, who don't have a clearly-articulated direction or if they do don't apply it to IT decisions.

2. Ensure your IT strategy and roadmap supports your business strategy. IT should not be an afterthought and IT decisions should not be based just on the internal requirement to get things done. All major IT decisions and investments should move the business in the desired direction and add to the bottom line, not subtract from it.

3. Understand what is important to your customers and how your IT helps you deliver this. All IT projects should improve the experience for your customers - possibly by improving the experience for your staff.

4. Having decided what you need IT to deliver then evaluate the impact of your choices about IT infrastructure and management on profit.

If you want to learn more about this then why not book online for this seminar on Using IT To Boost Business Performance?

My workshop programme covers this and every other key part of running a business, from strategy through to invoicing. For more details of this comprehensive and affordable course visit my business advice website.

If you'd like a free white paper on boosting the value of your company then complete this simple business value calculator

1. Set clear business direction as a prerequisite for the effective use of IT. This of course applies to the effective use of all parts of a business - marketing or operations or HR - but you'd be surprised at the number of companies, small and large, who don't have a clearly-articulated direction or if they do don't apply it to IT decisions.

2. Ensure your IT strategy and roadmap supports your business strategy. IT should not be an afterthought and IT decisions should not be based just on the internal requirement to get things done. All major IT decisions and investments should move the business in the desired direction and add to the bottom line, not subtract from it.

3. Understand what is important to your customers and how your IT helps you deliver this. All IT projects should improve the experience for your customers - possibly by improving the experience for your staff.

4. Having decided what you need IT to deliver then evaluate the impact of your choices about IT infrastructure and management on profit.

If you want to learn more about this then why not book online for this seminar on Using IT To Boost Business Performance?

My workshop programme covers this and every other key part of running a business, from strategy through to invoicing. For more details of this comprehensive and affordable course visit my business advice website.

If you'd like a free white paper on boosting the value of your company then complete this simple business value calculator

Monday, 1 November 2010

Manage your time, grow your profits

As a business owner or director your available time limits the growth and performance of your business unless you manage it properly.

How can you manage your time better?

- Schedule a weekly review with yourself. Set aside the same 15 minutes at the start or end of each week to write down the things that were achieved/missed in the past week and the things to be achieved in the next week

- Don’t just react to the latest stimulus. When a task or interruption appears, train yourself to decide what is urgent, what is important, what is both and what is neither and prioritise accordingly

- Start each day with a written list of things you are going to achieve that day and review the list at the end of the day

- Time-box your day - have targets for the next hour, by lunchtime, before I have a coffee...

- Set aside a time each day when you will accept NO distractions

- Have a schedule for everything that happens regularly - and stick to it

- Delegate everything unless there is a compelling reason not to. Aim to deskill tasks and process them using the lowest-cost resource. Taking responsibility for the things that distract you may well enrich the role of someone more junior

- Fix things for the long term. If you do have to break-off to deal with an unplanned issue don’t deal only with today’s interruption or distraction – understand the root cause and remove it, look at the trend and educate the people involved, set up simple processes, scripts, forms or rules to handle similar events in future

- Turn email alerts off. If you have an assistant, set them up with access to your email and get them to deal with everything they can, delete the junk and just leave the important stuff that you have to do yourself

- Set aside a time each day to deal with email – don’t look at it before that time and stop dealing with emails at the end of that period

Make sure that every day you have done something to make the business less reliant upon you.

My workshop programme covers this and every other key part of running a business, from strategy through to invoicing. For more details of this comprehensive and affordable course visit my business advice website.

If you'd like a free white paper on boosting the value of your company then complete this simple business value calculator

How can you manage your time better?

- Schedule a weekly review with yourself. Set aside the same 15 minutes at the start or end of each week to write down the things that were achieved/missed in the past week and the things to be achieved in the next week

- Don’t just react to the latest stimulus. When a task or interruption appears, train yourself to decide what is urgent, what is important, what is both and what is neither and prioritise accordingly

- Start each day with a written list of things you are going to achieve that day and review the list at the end of the day

- Time-box your day - have targets for the next hour, by lunchtime, before I have a coffee...

- Set aside a time each day when you will accept NO distractions

- Have a schedule for everything that happens regularly - and stick to it

- Delegate everything unless there is a compelling reason not to. Aim to deskill tasks and process them using the lowest-cost resource. Taking responsibility for the things that distract you may well enrich the role of someone more junior

- Fix things for the long term. If you do have to break-off to deal with an unplanned issue don’t deal only with today’s interruption or distraction – understand the root cause and remove it, look at the trend and educate the people involved, set up simple processes, scripts, forms or rules to handle similar events in future

- Turn email alerts off. If you have an assistant, set them up with access to your email and get them to deal with everything they can, delete the junk and just leave the important stuff that you have to do yourself

- Set aside a time each day to deal with email – don’t look at it before that time and stop dealing with emails at the end of that period

Make sure that every day you have done something to make the business less reliant upon you.

My workshop programme covers this and every other key part of running a business, from strategy through to invoicing. For more details of this comprehensive and affordable course visit my business advice website.

If you'd like a free white paper on boosting the value of your company then complete this simple business value calculator

Monday, 18 October 2010

How to deliver great customer service

Why is customer service so important?

- In the long run, good customer service is the only way to grow a successful business. Satisfied customers come back to buy more and also tell other potential customers about your service

- Good customer service forms a virtuous circle with employee satisfaction. People like to work for a business that they can be proud of and they like being able to make customers happy

- Poor service will produce the opposite effects and eventually destroy a business

What are the key elements in good customer service?

- Communication

o Understand your customer categories and the benefits they seek

o Engage customers in product development and service improvements

o Respond quickly and effectively to enquiries via the people who can provide the best solution to their need

o Agree with each client up-front what is to be delivered and how success will be measured

o Be accessible to customers at all their preferred times and using all their preferred channels

o Measure customer satisfaction regularly, publish the results and make sure the results provide a basis for action – then take it

- Culture

o Make explicit your values that tell everyone the customer is the top priority

o Train all employees in customer service and your values and then empower them to do what it takes to deliver great customer service

o Have an accessible complaints procedure focused on resolving the issue for all customers and all time

o Measure customer service and reward or acknowledge individuals who excel

o Do not tolerate poor customer service

- Processes and outcomes

o Define how you measure good customer service in your business and what key performance indicators (KPIs) are relevant for controlling the end-to-end process

o Include targets for these measures for all staff and review performance monthly and annually. Include them in your incentivisation scheme if you run one

o Publish actual performance figures against target

o Carry out regular and post-project reviews. Learn from mistakes and successes and capture improvements in revised processes

o Benchmark against the best performers inside and outside your industry

My workshop programme covers this and every other key part of running a business, from strategy through to invoicing. For more details of this comprehensive and affordable course visit my business advice website.

If you'd like a free white paper on boosting the value of your company then complete this simple business value calculator

- In the long run, good customer service is the only way to grow a successful business. Satisfied customers come back to buy more and also tell other potential customers about your service

- Good customer service forms a virtuous circle with employee satisfaction. People like to work for a business that they can be proud of and they like being able to make customers happy

- Poor service will produce the opposite effects and eventually destroy a business

What are the key elements in good customer service?

- Communication

o Understand your customer categories and the benefits they seek

o Engage customers in product development and service improvements

o Respond quickly and effectively to enquiries via the people who can provide the best solution to their need

o Agree with each client up-front what is to be delivered and how success will be measured

o Be accessible to customers at all their preferred times and using all their preferred channels

o Measure customer satisfaction regularly, publish the results and make sure the results provide a basis for action – then take it

- Culture

o Make explicit your values that tell everyone the customer is the top priority

o Train all employees in customer service and your values and then empower them to do what it takes to deliver great customer service

o Have an accessible complaints procedure focused on resolving the issue for all customers and all time

o Measure customer service and reward or acknowledge individuals who excel

o Do not tolerate poor customer service

- Processes and outcomes

o Define how you measure good customer service in your business and what key performance indicators (KPIs) are relevant for controlling the end-to-end process

o Include targets for these measures for all staff and review performance monthly and annually. Include them in your incentivisation scheme if you run one

o Publish actual performance figures against target

o Carry out regular and post-project reviews. Learn from mistakes and successes and capture improvements in revised processes

o Benchmark against the best performers inside and outside your industry

My workshop programme covers this and every other key part of running a business, from strategy through to invoicing. For more details of this comprehensive and affordable course visit my business advice website.

If you'd like a free white paper on boosting the value of your company then complete this simple business value calculator

Monday, 4 October 2010

How resilient is your turnover?

Not all revenue is equally certain. A business which relies on winning a small number of large contracts each year may well earn the same revenue and profit as a business that gets its income from a large volume of contracted subscriptions and a third company that gets all its income from ad-hoc repair and maintenance across a moderate number of existing customers

o In theory, the riskier nature of the project business should result in higher profit margins (returns to the shareholders) and the stable nature of the subscription business, lower - but this is not always the case in practice

o Don’t confuse spreading payments for a project with spreading both the cost and the income by using a different business model. The first impacts cash flow and actually increases risk – so should require an even higher return.

All other things being equal, businesses should strive for as much locked-in recurring revenue as possible

How can you translate one-off into recurring revenue? Some examples of spreading payments are

o A photocopier which is paid for by charging a small amount for every copy made

o Mobile phones, where the phone is given free in return for a fixed term monthly contract

Each of these relies on a higher total income over the life of the contract to cover the cash flow hit and the risk of default. It is also necessary to build in a compelling proposition to renew the contract before it expires in order to build revenue resilience

Some examples of additional recurring revenue are

o Software license maintenance

o Membership of a user group

o Subscription services

o Service and maintenance contracts

An alternative way of looking at this is separating future income from resource or asset limitations

o Translate a single consultant’s time into a course to be sold online in perpetuity

What is the proposition for the customer? Possible benefits that would induce a customer to sign up for a long-term contract are

o Access to a continuous stream of new content

o Access to special offers and discounts

o A known fixed charge covering all repairs (a form of insurance)

o The right to free future upgrades

o Continuous tuning & maintenance of the original product

One final source of revenue risk is over-reliance on a single or a few customers (high customer concentration) – avoid this.

See how I can make your business more profitable.

See how my services could make your business worth more

Want to see videos of my seminars for business owners?

o In theory, the riskier nature of the project business should result in higher profit margins (returns to the shareholders) and the stable nature of the subscription business, lower - but this is not always the case in practice

o Don’t confuse spreading payments for a project with spreading both the cost and the income by using a different business model. The first impacts cash flow and actually increases risk – so should require an even higher return.

All other things being equal, businesses should strive for as much locked-in recurring revenue as possible

How can you translate one-off into recurring revenue? Some examples of spreading payments are

o A photocopier which is paid for by charging a small amount for every copy made

o Mobile phones, where the phone is given free in return for a fixed term monthly contract

Each of these relies on a higher total income over the life of the contract to cover the cash flow hit and the risk of default. It is also necessary to build in a compelling proposition to renew the contract before it expires in order to build revenue resilience

Some examples of additional recurring revenue are

o Software license maintenance

o Membership of a user group

o Subscription services

o Service and maintenance contracts

An alternative way of looking at this is separating future income from resource or asset limitations

o Translate a single consultant’s time into a course to be sold online in perpetuity

What is the proposition for the customer? Possible benefits that would induce a customer to sign up for a long-term contract are

o Access to a continuous stream of new content

o Access to special offers and discounts

o A known fixed charge covering all repairs (a form of insurance)

o The right to free future upgrades

o Continuous tuning & maintenance of the original product

One final source of revenue risk is over-reliance on a single or a few customers (high customer concentration) – avoid this.

See how I can make your business more profitable.

See how my services could make your business worth more

Want to see videos of my seminars for business owners?

Wednesday, 22 September 2010

Why systemised businesses are worth more

The value of a business depends on its growth prospects, profitability, cash conversion and the degree to which that future cash flow is at risk

o One of the main risks for small businesses is their reliance upon key personnel, particularly the owner, who know and do things that no-one else knows or can do

o This risk is present even if you have no plans to sell the business. If you the owner or one of your key staff are unable to work for an extended period what happens to your business?

o Systemisation is the process by which the processes of the business are documented and standardised and reliance on any one individual is removed

o This process also makes a business scalable; the processes can be replicated, additional staff can be selected and trained and the business can grow beyond the constraints of any one person

How can a business be systemised?

- Document all your processes. Start by asking all your staff (including you) what they spend their time doing and build up a diagram of the different flows of work from the start (say a customer enquiry) to the end (say an invoice paid)

o Post-it notes are a good way to do this. Use different colours for different people or departments and put a different task on each note. Record key dimensions on each task – how many times, how often, how long it takes. Record problems or issues with the task. Organise the notes into sequences of tasks (processes)

o Turn the hierarchy and sequence of notes into your draft written operating manual

- Identify where only one person has the skills to carry out a particular task and examine ways to enable more people to do this

o Delegation and recruitment

o Training

o Cross-skilling, so that people can turn their hand to multiple roles

o Altering the task so that it becomes less specialised

- Look for opportunities to improve processes

o Complexity that has arisen for no good reason over time

o Bottlenecks

o Different ways of carrying out what is essentially the same task

o Specialised resources being used for mundane tasks

- Automate where this is practical

o Streamline and speed processes up using computers and the internet

o Look for opportunities to provide self-service – this reduces cost and improves customer service

- Finalise and issue the operating manual

o Institute regular audits to ensure the manual and the reality match

- Starting with you, the owner, develop a succession plan

o Named individuals selected or recruited to replace the people above them

o The appropriate development plans in place for these individuals

See how my services could help your business.

See how my services could make your business worth more

Want to see videos of my seminars for business owners?

o One of the main risks for small businesses is their reliance upon key personnel, particularly the owner, who know and do things that no-one else knows or can do

o This risk is present even if you have no plans to sell the business. If you the owner or one of your key staff are unable to work for an extended period what happens to your business?

o Systemisation is the process by which the processes of the business are documented and standardised and reliance on any one individual is removed

o This process also makes a business scalable; the processes can be replicated, additional staff can be selected and trained and the business can grow beyond the constraints of any one person

How can a business be systemised?

- Document all your processes. Start by asking all your staff (including you) what they spend their time doing and build up a diagram of the different flows of work from the start (say a customer enquiry) to the end (say an invoice paid)

o Post-it notes are a good way to do this. Use different colours for different people or departments and put a different task on each note. Record key dimensions on each task – how many times, how often, how long it takes. Record problems or issues with the task. Organise the notes into sequences of tasks (processes)

o Turn the hierarchy and sequence of notes into your draft written operating manual

- Identify where only one person has the skills to carry out a particular task and examine ways to enable more people to do this

o Delegation and recruitment

o Training

o Cross-skilling, so that people can turn their hand to multiple roles

o Altering the task so that it becomes less specialised

- Look for opportunities to improve processes

o Complexity that has arisen for no good reason over time

o Bottlenecks

o Different ways of carrying out what is essentially the same task

o Specialised resources being used for mundane tasks

- Automate where this is practical

o Streamline and speed processes up using computers and the internet

o Look for opportunities to provide self-service – this reduces cost and improves customer service

- Finalise and issue the operating manual

o Institute regular audits to ensure the manual and the reality match

- Starting with you, the owner, develop a succession plan

o Named individuals selected or recruited to replace the people above them

o The appropriate development plans in place for these individuals

See how my services could help your business.

See how my services could make your business worth more

Want to see videos of my seminars for business owners?

Wednesday, 15 September 2010

Improving productivity

What is meant by “productivity”?

- Productivity is a measure of output for some measure of input

- Productivity has huge impact on profitability as shown in the table

- This approach applies to services as well as products

How can productivity be improved?

- Decide what it is you produce (the output) – this may not be obvious in a service business

- Identify the main costs or resources utilised in production (the inputs)

- Define your productivity measure(s) – in the above table it is labour hours/item

- Monitor productivity over time and between different employees or resources

- If the main productivity factor is labour then improvements can be made in training, supervision, communication, standardisation, documentation, tools, systems or support

- For non-labour measures examine product or process design

See how my services could help your business.

See how my services could make your business worth more

Want to see videos of my seminars for business owners?

- Productivity is a measure of output for some measure of input

- Maintenance visits per hour of direct labour

- Cakes sold per hour of shop assistant labour

- Boxes produced per square metre of steel

- Helpdesk calls closed per man-month

- For your business you can choose whatever measures are most useful

- Productivity has huge impact on profitability as shown in the table

- The company has 8,000 hours per year of productive labour. The budget is based on these hours producing 100 items which results in a 10% profit.

- A 10% improvement in productivity (each person on average producing 10% more in a given period) results in a doubling of profit

- A 10% deterioration in productivity results in no profit being made at all

- This approach applies to services as well as products

How can productivity be improved?

- Decide what it is you produce (the output) – this may not be obvious in a service business

- Identify the main costs or resources utilised in production (the inputs)

- Define your productivity measure(s) – in the above table it is labour hours/item

- Monitor productivity over time and between different employees or resources

- If the main productivity factor is labour then improvements can be made in training, supervision, communication, standardisation, documentation, tools, systems or support

- For non-labour measures examine product or process design

Monday, 6 September 2010

Market triggers

What are market triggers?

- Most products and services have some kind of event that triggers the customer need

- These triggers may be seasonal (school uniform, umbrellas), calendar-driven (payroll, VAT returns) or ad-hoc (marriage, moving house)

Why should you understand your market triggers?

- Understanding your market triggers will help you to position your product or service where it is most likely to catch the customer at the right time or place

o If you run a carpet cleaning company then demand for your services might be triggered by someone moving into a new home – so post leaflets through the doors of houses with “sold” signs

o If you print business cards and stationary then demand for your services might be triggered by someone setting up a new company – so subscribe to a company registration data service and send start-ups a brochure

- Understanding the customer motivation will help you best meet their needs and so improve sales conversion rate

o Make it part of scripts and qualification to ask why the prospect is looking for your product or service

- It will help you cross-sell or up-sell other services related to the trigger

o Someone who gets divorced may well need a new will

o Someone who hires a lot of new staff may well need employment policies

- It will suggest related complementary services and so which strategic alliances would be beneficial to you

o Solicitors will form alliances with estate agents to get access to conveyancing work

See how my services could help your business.

See how my services could make your business worth more

Want to see videos of my seminars for business owners?

- Most products and services have some kind of event that triggers the customer need

- These triggers may be seasonal (school uniform, umbrellas), calendar-driven (payroll, VAT returns) or ad-hoc (marriage, moving house)

Why should you understand your market triggers?

- Understanding your market triggers will help you to position your product or service where it is most likely to catch the customer at the right time or place

o If you run a carpet cleaning company then demand for your services might be triggered by someone moving into a new home – so post leaflets through the doors of houses with “sold” signs

o If you print business cards and stationary then demand for your services might be triggered by someone setting up a new company – so subscribe to a company registration data service and send start-ups a brochure

- Understanding the customer motivation will help you best meet their needs and so improve sales conversion rate

o Make it part of scripts and qualification to ask why the prospect is looking for your product or service

- It will help you cross-sell or up-sell other services related to the trigger

o Someone who gets divorced may well need a new will

o Someone who hires a lot of new staff may well need employment policies

- It will suggest related complementary services and so which strategic alliances would be beneficial to you

o Solicitors will form alliances with estate agents to get access to conveyancing work

See how my services could help your business.

See how my services could make your business worth more

Want to see videos of my seminars for business owners?

Tuesday, 24 August 2010

A big sales technique for small businesses

- Consultative selling, or solutions selling , is a technique used by big companies for complex sales. However, it can be used by SMEs for business-to-business (B2B) or even business-to-consumer (B2C) selling. The essence is to go beyond the stated requirement to understand your prospects’ needs and explain how your product or service meets those needs better than anyone else’s.

Preparation:

- Research on the customer (for B2B - turnover, growth, products, stated aims, stated strategies, culture and strengths. For B2C – the benefits your various customer types are looking for);

- Research on the market (emerging trends, main players, size, growing/shrinking, macro-economic factors eg is the market driven by the housing market or unemployment);

Set the scene:

- For planned meetings send an agenda/have a pre-meeting telephone call that sets the expectation that you are interested in how your product or service can help the prospect achieve their aims – you are not turning up to talk about features or technology

- For unplanned (eg in a shop) make sure you have a script that engages the prospect in a discussion about their needs

The discussion:

- For B2B, set out to understand the following things:

o What the company produces

o How many/how much they produce

o What is important to their customers

o What is their USP?

o How do they get the best from their staff?

o What are the top three challenges they are facing?

- For B2C, set out to understand the experience they are seeking

o In a shoe shop, don’t ask “Can I help you?” ask “Are you looking for shoes with a special event in mind?”

o If someone rings about a new carpet ask them “What does the room feel like?” or “What atmosphere are you trying to create?”

- Explore with open questions (that require a descriptive answer) and confirm your understanding with closed questions (that can be answered Yes or No)

- Listen, listen, listen

- Explain to them how your product or service helps them achieve this

o Point by point match benefit to need

o Use their own language

o Don’t assume they will recognise all the benefits you are offering without you telling them

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

Preparation:

- Research on the customer (for B2B - turnover, growth, products, stated aims, stated strategies, culture and strengths. For B2C – the benefits your various customer types are looking for);

- Research on the market (emerging trends, main players, size, growing/shrinking, macro-economic factors eg is the market driven by the housing market or unemployment);

Set the scene:

- For planned meetings send an agenda/have a pre-meeting telephone call that sets the expectation that you are interested in how your product or service can help the prospect achieve their aims – you are not turning up to talk about features or technology

- For unplanned (eg in a shop) make sure you have a script that engages the prospect in a discussion about their needs

The discussion:

- For B2B, set out to understand the following things:

o What the company produces

o How many/how much they produce

o What is important to their customers

o What is their USP?

o How do they get the best from their staff?

o What are the top three challenges they are facing?

- For B2C, set out to understand the experience they are seeking

o In a shoe shop, don’t ask “Can I help you?” ask “Are you looking for shoes with a special event in mind?”

o If someone rings about a new carpet ask them “What does the room feel like?” or “What atmosphere are you trying to create?”

- Explore with open questions (that require a descriptive answer) and confirm your understanding with closed questions (that can be answered Yes or No)

- Listen, listen, listen

- Explain to them how your product or service helps them achieve this

o Point by point match benefit to need

o Use their own language

o Don’t assume they will recognise all the benefits you are offering without you telling them

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

Monday, 16 August 2010

Why qualifying sales will help sales grow

Why do you need to qualify sales leads?

- The process which takes a lead through to a sale (the conversion process) can consume a lot of resources, particularly for complex sales

- This process is much more productive (that is, has a higher conversion rate and uses less resource) if those leads which are likely to be low value and/or unlikely to result in a sale are screened out earlier in the process

- If the conversion process has very low marginal costs (eg an online shop) then the need for qualification is correspondingly lower

What factors can be used to qualify sales leads?

- The factors can vary widely according to the industry you are in but could include:

o Are you talking to the decision-maker and budget-holder?

o Are they in your target market and the right type and size of customer?

o Do they have the funds or budget to buy your product?

o Do they have the compelling need, commitment and motivation to buy now?

o Can you provide what they need without stretching your product, credibility or resources?

o Do you have all the necessary pre-qualifications (policies, accreditations, size and stability)?

o Is there an incumbent or preferred supplier who is almost certain to win the business?

How are leads qualified?

- Qualification should be part of your sales process

o It should also be built into your marketing

- It could take place at a single point or you could have several stages of qualification

- The criteria for qualification (taken, for example, from the above list) should be recorded against each lead in your sales management system

- The conversion process results (wins and losses) should feed back into the qualification process

o A low conversion rate may well indicate poor qualification

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

- The process which takes a lead through to a sale (the conversion process) can consume a lot of resources, particularly for complex sales

- This process is much more productive (that is, has a higher conversion rate and uses less resource) if those leads which are likely to be low value and/or unlikely to result in a sale are screened out earlier in the process

- If the conversion process has very low marginal costs (eg an online shop) then the need for qualification is correspondingly lower

What factors can be used to qualify sales leads?

- The factors can vary widely according to the industry you are in but could include:

o Are you talking to the decision-maker and budget-holder?

o Are they in your target market and the right type and size of customer?

o Do they have the funds or budget to buy your product?

o Do they have the compelling need, commitment and motivation to buy now?

o Can you provide what they need without stretching your product, credibility or resources?

o Do you have all the necessary pre-qualifications (policies, accreditations, size and stability)?

o Is there an incumbent or preferred supplier who is almost certain to win the business?

How are leads qualified?

- Qualification should be part of your sales process

o It should also be built into your marketing

- It could take place at a single point or you could have several stages of qualification

- The criteria for qualification (taken, for example, from the above list) should be recorded against each lead in your sales management system

- The conversion process results (wins and losses) should feed back into the qualification process

o A low conversion rate may well indicate poor qualification

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

Tuesday, 10 August 2010

Why do so many small businesses fail?

Why do so many small businesses fail?

This topic generated over 50 comments on a LinkedIn forum recently. This counts as a furore in the restrained atmosphere of LinkedIn Groups.

Comments came from a range of business owners, with perhaps a preponderance of those who advise other businesses. Whilst this skewed the comments made it also ensured that there was considerable experience of the reasons why UK SMEs survive or fail.

I counted up the reasons put forward – a completely unscientific analysis of a self-selecting group but interesting nevertheless. The reasons put forward were:

1. Owner's attitude/mental strength/direction/native ability/intelligence (8 mentions)

2. Business management knowledge and willingness to take advice (7 mentions)

3. Sales ability (6 mentions)

4. Financial understanding and control, particularly of cash flow (6 mentions)

5. USP/great idea or product, effective market research (5 mentions)

6. Business planning (3 mentions)

Also mentioned were: Customer understanding, luck, banks, pricing and contracts.

Not the ranking I would have come up with at the start I must confess. It prompts the question: If this ranking is reflective of anything like the actual reasons, what interventions are actually likely to be most effective?

Postscript: Whilst preparing this blog I met the owner of a design and branding company who is in his tenth year of business and expecting to turnover £1.5m this year. He and his partner have been using the latest of a series of advisors for the last 9 months - a series which started with a mentor when they set up the business. We talked about their plans to take on a shared FD shortly - not to control the finances but to raise their strategic game.

Perhaps businesses that are smart enough to know when they need advice and are willing to invest in it stand a better chance of survival.

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

This topic generated over 50 comments on a LinkedIn forum recently. This counts as a furore in the restrained atmosphere of LinkedIn Groups.

Comments came from a range of business owners, with perhaps a preponderance of those who advise other businesses. Whilst this skewed the comments made it also ensured that there was considerable experience of the reasons why UK SMEs survive or fail.

I counted up the reasons put forward – a completely unscientific analysis of a self-selecting group but interesting nevertheless. The reasons put forward were:

1. Owner's attitude/mental strength/direction/native ability/intelligence (8 mentions)

2. Business management knowledge and willingness to take advice (7 mentions)

3. Sales ability (6 mentions)

4. Financial understanding and control, particularly of cash flow (6 mentions)

5. USP/great idea or product, effective market research (5 mentions)

6. Business planning (3 mentions)

Also mentioned were: Customer understanding, luck, banks, pricing and contracts.

Not the ranking I would have come up with at the start I must confess. It prompts the question: If this ranking is reflective of anything like the actual reasons, what interventions are actually likely to be most effective?

Postscript: Whilst preparing this blog I met the owner of a design and branding company who is in his tenth year of business and expecting to turnover £1.5m this year. He and his partner have been using the latest of a series of advisors for the last 9 months - a series which started with a mentor when they set up the business. We talked about their plans to take on a shared FD shortly - not to control the finances but to raise their strategic game.

Perhaps businesses that are smart enough to know when they need advice and are willing to invest in it stand a better chance of survival.

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

Monday, 26 July 2010

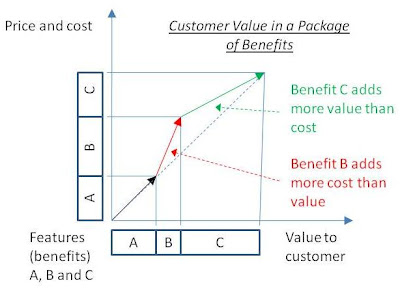

Customer benefits and their costs

A customer buys a package of benefits when they buy your product or service

- Some of these benefits are more important than others to your customer – some they may not want or value at all, some are critical and some they may not even realise they get. This will be different for each customer

- Some of these benefits cost you more than others to provide – some cost you a lot and some are free – or may even reduce your costs

- If you understand the relative value and cost then this allows you to make adjustments to your product, pricing and proposition so that you optimise revenue and margin

o This is the basis of the low-cost airline model. The benefits that were removed were valued less by passengers than the price reduction made possible by re-designing the airline process

How can I use this in my small business?

- Make sure that you understand all the benefits included in your product or service and that they are highlighted in your proposition

- If appropriate, develop different services to incorporate different packages of benefits (gold, silver and bronze for instance)

- In individual cases, understanding relative costs and benefits will help you negotiate with the customer

o You can make sure that they are comparing like with like in terms of the complete benefits package by you and your competition

o You can discuss which benefits they are prepared to forgo if they are asking for a price reduction

o You can offer additional benefits that cost you little or nothing but which the customer values in order to close a deal

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

- Some of these benefits are more important than others to your customer – some they may not want or value at all, some are critical and some they may not even realise they get. This will be different for each customer

- Some of these benefits cost you more than others to provide – some cost you a lot and some are free – or may even reduce your costs

- If you understand the relative value and cost then this allows you to make adjustments to your product, pricing and proposition so that you optimise revenue and margin

o This is the basis of the low-cost airline model. The benefits that were removed were valued less by passengers than the price reduction made possible by re-designing the airline process

How can I use this in my small business?

- Make sure that you understand all the benefits included in your product or service and that they are highlighted in your proposition

- If appropriate, develop different services to incorporate different packages of benefits (gold, silver and bronze for instance)

- In individual cases, understanding relative costs and benefits will help you negotiate with the customer

o You can make sure that they are comparing like with like in terms of the complete benefits package by you and your competition

o You can discuss which benefits they are prepared to forgo if they are asking for a price reduction

o You can offer additional benefits that cost you little or nothing but which the customer values in order to close a deal

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

Monday, 19 July 2010

Why a business owner needs vision

Why have a Vision Statement?

- The purpose of creating a Vision Statement is to provide you, the business owner, with a clear picture of what you are going to achieve through owning your business

- One of the seven habits of effective leaders (as defined by Steven Covey) is that they always start with the end in mind. Even if your eventual exit from your business is many years away it will be worth far more and the exit process will be far easier if everything you do contributes to that exit

- If you do not have a clear vision how will you know which path to take or which decision to make? A clear vision will help you make those key decisions along the way

- The vision for your business will help you set short, mid and long-term objectives. When you set those objectives you should ask yourself how they contribute to achieving your vision

- The vision for your business will help you evaluate how you spend your time. Ask yourself frequently “How does this activity help me achieve my vision?” If it doesn’t, why are you doing it?

- It will help you communicate what is different and better about your business to staff and customers

What makes a good Vision Statement?

- It must be motivating for you. It must be something that you think is worth achieving and which matches your values and beliefs

- It should describe a particular point in time. This might be when you plan to exit or when you plan to achieve “success” as you see it. It should have a date

- It should describe what the business will be in concrete terms – how large, what it will be known for, what it will be able to do

- It should have a personal goal that describes how you will be spending your life. This might include your working life or your personal life or the options you would have by then

- It should have some concrete financial dimension – usually sale value, turnover or profit

- It should be written down

What do you do with your Vision Statement when you’ve got one?

- Use it to develop your internal and external Mission Statements which communicate to staff and customers what it is you do and why. (You wouldn’t normally share your Vision Statement directly with anyone else)

- Read it frequently. Use visioning or affirmations to picture yourself and your business at the point of the vision and look backwards at all the choices you made, the successes you had and the obstacles you overcame to get there – starting with the things you are doing today

- Use it to set your short, medium and long-term objectives and to validate your current strategy and decisions

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

- The purpose of creating a Vision Statement is to provide you, the business owner, with a clear picture of what you are going to achieve through owning your business

- One of the seven habits of effective leaders (as defined by Steven Covey) is that they always start with the end in mind. Even if your eventual exit from your business is many years away it will be worth far more and the exit process will be far easier if everything you do contributes to that exit

- If you do not have a clear vision how will you know which path to take or which decision to make? A clear vision will help you make those key decisions along the way

- The vision for your business will help you set short, mid and long-term objectives. When you set those objectives you should ask yourself how they contribute to achieving your vision

- The vision for your business will help you evaluate how you spend your time. Ask yourself frequently “How does this activity help me achieve my vision?” If it doesn’t, why are you doing it?

- It will help you communicate what is different and better about your business to staff and customers

What makes a good Vision Statement?

- It must be motivating for you. It must be something that you think is worth achieving and which matches your values and beliefs

- It should describe a particular point in time. This might be when you plan to exit or when you plan to achieve “success” as you see it. It should have a date

- It should describe what the business will be in concrete terms – how large, what it will be known for, what it will be able to do

- It should have a personal goal that describes how you will be spending your life. This might include your working life or your personal life or the options you would have by then

- It should have some concrete financial dimension – usually sale value, turnover or profit

- It should be written down

What do you do with your Vision Statement when you’ve got one?

- Use it to develop your internal and external Mission Statements which communicate to staff and customers what it is you do and why. (You wouldn’t normally share your Vision Statement directly with anyone else)

- Read it frequently. Use visioning or affirmations to picture yourself and your business at the point of the vision and look backwards at all the choices you made, the successes you had and the obstacles you overcame to get there – starting with the things you are doing today

- Use it to set your short, medium and long-term objectives and to validate your current strategy and decisions

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

Monday, 12 July 2010

Why customers leave

- The most-often quoted study is one attributed to, variously, The American Society for Quality, the US Chambers of Commerce and a book called “Lessons from the Field” by Howard Feiertag and John Hogan. This gives the following reasons for customers leaving:

o Death or moving away – 4%

o The influence of friends and relatives – 5%

o Competitor marketing and special offers – 9%

o Dissatisfaction with product or price – 14%

o Perceived indifference of the supplier – 68%

- A study by RightNow Technologies says

o 73% of customers leave because of poor customer service but the supplier thinks that only 21% leave because of customer service

o The supplier thinks 48% leave because of price when in fact only 25% do so

- Mercer Management Consulting research shows that for a selection of retail outlets, only 15% to 30% of customers are price sensitive – that is, they would change supplier for a better price

- So retaining customers is not (usually) about price – it’s about letting the customer know you care

So if you love your customers can you charge what you like?

- No. You have to be competitive in your market - but superior customer care and marketing mix (USP, positioning and so forth) means you get to keep most of your customers and still charge a premium

- Low prices won’t keep customers if they think you are indifferent to them. Worse, using low prices attracts disloyal customers. The worst strategy of all is using low prices to make up for the fact that you and your staff really don’t care

It’s really difficult and expensive to get all my staff to provide great customer service

- It might seem so to start with – but the rewards are huge

o According to a study by the global business consulting firm Baines a 5% increase in customer retention can increase a company’s profitability by 75%

o Reichheld and Sasser reported that when MBNA America reduced its 10% defection rate to 5% their profits rose by 125%

- What we’re really talking about is values and beliefs. It’s the way you behave and what gets measured and what gets rewarded.

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

o Death or moving away – 4%

o The influence of friends and relatives – 5%

o Competitor marketing and special offers – 9%

o Dissatisfaction with product or price – 14%

o Perceived indifference of the supplier – 68%

- A study by RightNow Technologies says

o 73% of customers leave because of poor customer service but the supplier thinks that only 21% leave because of customer service

o The supplier thinks 48% leave because of price when in fact only 25% do so

- Mercer Management Consulting research shows that for a selection of retail outlets, only 15% to 30% of customers are price sensitive – that is, they would change supplier for a better price

- So retaining customers is not (usually) about price – it’s about letting the customer know you care

So if you love your customers can you charge what you like?

- No. You have to be competitive in your market - but superior customer care and marketing mix (USP, positioning and so forth) means you get to keep most of your customers and still charge a premium

- Low prices won’t keep customers if they think you are indifferent to them. Worse, using low prices attracts disloyal customers. The worst strategy of all is using low prices to make up for the fact that you and your staff really don’t care

It’s really difficult and expensive to get all my staff to provide great customer service

- It might seem so to start with – but the rewards are huge

o According to a study by the global business consulting firm Baines a 5% increase in customer retention can increase a company’s profitability by 75%

o Reichheld and Sasser reported that when MBNA America reduced its 10% defection rate to 5% their profits rose by 125%

- What we’re really talking about is values and beliefs. It’s the way you behave and what gets measured and what gets rewarded.

More business advice for business owners.

How do you value your business?

Want to see videos of my seminars for business owners?

Monday, 5 July 2010

Why do you need job description?

Why have job descriptions?

- Job descriptions are an essential part of co-ordinating and motivating employees

- Without a job description an employee does not have a clear understanding of what they are supposed to achieve and how their performance is measured – and you have no way to hold them accountable

- The process of creating and reviewing job descriptions is an opportunity to discuss and clarify the role – to reinforce two-way communication

What should be in a job description?

- Job Title

- The role that the position reports to (not the person)

- Main purpose of the role. One or two sentences that describe the main output of the job.

- Responsibilities

o The tasks and deliverables of the role - keep this to a maximum of six

o One sentence each

o Include only the permanent elements of the role – not transient targets or projects

o Be generic rather than specific: “Conform to current operations procedures “ rather than “Carry out procedures x, y and z”. Do not duplicate procedures or manuals.

- Dimensions

o The budget controlled

o Number of direct reports

o Regional or product boundaries

- Key challenges of the role

- Performance measures

o The key deliverables: “Performance against sales target” or “Customer satisfaction score”

o Keep this to a maximum of four

o Don’t include actual targets – these may change

- Required attributes

o Technical knowledge or skills

o Experience and qualifications

o Personal strengths: “Able to work on own initiative” or “Aptitude with technology”

Implementing job descriptions

- Use a standard template – or possibly two, one for management and one for other roles

- Where a new job description is required then get the post-holder to write it using the standard template (you still need to review and own it)

- Use generic job descriptions where you have more than one person doing the same job

- It gets more difficult to write a job description the more junior the role. It is difficult sometimes to identify performance measures for a clerical assistant. Nevertheless, if you are to develop a high-performance team then every employee needs to understand what they are supposed to be doing and how their performance will be measured

- Job descriptions should be no longer than one side of A4 - try these employment templates

More business advice for business owners.

How do I value my business?

Want to see videos giving business advice in Berkshire and Reading?

- Job descriptions are an essential part of co-ordinating and motivating employees

- Without a job description an employee does not have a clear understanding of what they are supposed to achieve and how their performance is measured – and you have no way to hold them accountable

- The process of creating and reviewing job descriptions is an opportunity to discuss and clarify the role – to reinforce two-way communication

What should be in a job description?

- Job Title

- The role that the position reports to (not the person)

- Main purpose of the role. One or two sentences that describe the main output of the job.

- Responsibilities

o The tasks and deliverables of the role - keep this to a maximum of six

o One sentence each

o Include only the permanent elements of the role – not transient targets or projects

o Be generic rather than specific: “Conform to current operations procedures “ rather than “Carry out procedures x, y and z”. Do not duplicate procedures or manuals.

- Dimensions

o The budget controlled

o Number of direct reports

o Regional or product boundaries

- Key challenges of the role

- Performance measures

o The key deliverables: “Performance against sales target” or “Customer satisfaction score”

o Keep this to a maximum of four

o Don’t include actual targets – these may change

- Required attributes

o Technical knowledge or skills

o Experience and qualifications

o Personal strengths: “Able to work on own initiative” or “Aptitude with technology”

Implementing job descriptions

- Use a standard template – or possibly two, one for management and one for other roles

- Where a new job description is required then get the post-holder to write it using the standard template (you still need to review and own it)

- Use generic job descriptions where you have more than one person doing the same job

- It gets more difficult to write a job description the more junior the role. It is difficult sometimes to identify performance measures for a clerical assistant. Nevertheless, if you are to develop a high-performance team then every employee needs to understand what they are supposed to be doing and how their performance will be measured

- Job descriptions should be no longer than one side of A4 - try these employment templates

More business advice for business owners.

How do I value my business?

Want to see videos giving business advice in Berkshire and Reading?

Tuesday, 29 June 2010

Is business growth optional?

An acquaintance and business owner emailed me: "...I've never understood why business people are so obsessed with [growth], it just seems like an option to me...". He is not alone - a significant proportion of owner-managers with whom I work or who come to my business seminars are averse to growing their business. Often the reasons put forward are lifestyle choice, reluctance to employ more staff or fear that quality will suffer.

Now some of these are sole-traders or single consultants for which the term self-employed is more appropriate. The comments below refer to business owners, by which I mean people who employ and organise staff.

Here are my reasons, in no particular order, for suggesting that growth is necessary for an owner-managed business:

1. To be compelling for staff an organisation has to have a vision of something bigger than just the people involved. They want to be on a meaningful journey;

2. An organisation has to adapt, evolve and learn in order to survive in a changing environment. Whilst a smaller organisation may be more agile, often developing additional capabilities and skills requires new people and to do it well and consistently requires the size to cover the costs of developmental resources (that is, resources not completely utilised in production);

3. The bigger members of a species generally get the most food and their pick of mates. Business is an ecosystem and, all other things being equal, you will lose to your bigger competitors in the long run as they improve margins through economies of scale and spend more on marketing, product development and so forth;

4. There are economies of scale at all levels within an industry (so even small companies should operate more efficiently than their still smaller competitors);

5. Even if you have a unique advantage over your competition it is advisable to sell more, invest in developing that advantage and so exclude competition from that space - or risk losing the advantage. In this way a behaviour aimed at survival leads to growth;

6. Investment (whether angel, pension funds or bank loans) will follow the best returns. Whilst a private company does not have the exposure of a plc, in the long run growth means better returns and so easier access to funds. Even if a business owner is not seeking external funding, he or she takes the decision to invest more in their business every day. Rational behaviour is surely to seek increasingly good returns from that investment.

So growth may or may not be an end in itself but it is always a by-product for businesses that are fit to survive and in turn makes businesses more likely to survive. Business owners who decline to take on the very real challenges of making growth happen are not only unlikely to achieve the latent value in their business but also run the risk that they will not be one of the fittest that survive.

So...is business growth optional? Of course. So is learning to swim.

For more business advice for business owners go here

Want to know how much your company is worth (and why)? Go here

Now some of these are sole-traders or single consultants for which the term self-employed is more appropriate. The comments below refer to business owners, by which I mean people who employ and organise staff.

Here are my reasons, in no particular order, for suggesting that growth is necessary for an owner-managed business:

1. To be compelling for staff an organisation has to have a vision of something bigger than just the people involved. They want to be on a meaningful journey;

2. An organisation has to adapt, evolve and learn in order to survive in a changing environment. Whilst a smaller organisation may be more agile, often developing additional capabilities and skills requires new people and to do it well and consistently requires the size to cover the costs of developmental resources (that is, resources not completely utilised in production);

3. The bigger members of a species generally get the most food and their pick of mates. Business is an ecosystem and, all other things being equal, you will lose to your bigger competitors in the long run as they improve margins through economies of scale and spend more on marketing, product development and so forth;

4. There are economies of scale at all levels within an industry (so even small companies should operate more efficiently than their still smaller competitors);

5. Even if you have a unique advantage over your competition it is advisable to sell more, invest in developing that advantage and so exclude competition from that space - or risk losing the advantage. In this way a behaviour aimed at survival leads to growth;

6. Investment (whether angel, pension funds or bank loans) will follow the best returns. Whilst a private company does not have the exposure of a plc, in the long run growth means better returns and so easier access to funds. Even if a business owner is not seeking external funding, he or she takes the decision to invest more in their business every day. Rational behaviour is surely to seek increasingly good returns from that investment.

So growth may or may not be an end in itself but it is always a by-product for businesses that are fit to survive and in turn makes businesses more likely to survive. Business owners who decline to take on the very real challenges of making growth happen are not only unlikely to achieve the latent value in their business but also run the risk that they will not be one of the fittest that survive.

So...is business growth optional? Of course. So is learning to swim.

For more business advice for business owners go here

Want to know how much your company is worth (and why)? Go here

Monday, 21 June 2010

Competitive Intelligence

What is competitive intelligence?

- In order to compete with and beat your competitors you need to know and understand them

- Large companies take a very methodical approach to this and may use specialist CI providers

- Lots of different pieces of information are put together to produce a picture of the competitors strengths, weaknesses, performance and intentions

- The principles can be simplified and used by small businesses

Why do you need competitive intelligence?

- To pick up new products and trends in your market

- To identify new markets

- To improve your understanding of what is important to your customers

- To adjust your proposition and positioning to make the most of relative strengths and weaknesses

- To take advantage of opportunities such as competitor failure

How do you gather competitive intelligence?

Online

o Their website

o Social media sites

o Newspapers

o Filings (Companies House)

o Job ads

o Press releases

Offline

o Their marketing materials, brochures, pricelists

o Trade shows

o Suppliers/partners/sub-contractors

o Their customers, your customer surveys

o Trade press

How should you do this in a small business?

- Keep a simple file of information you pick up about your key competitors

- Periodically, plan time to do a few hours research on them

- Periodically, plan time to review your proposition and positioning against this information using Competitor Analysis

- Adjust your proposition and look at the new opportunities suggested

For more business advice for business owners go here

Want to know how much your company is worth (and why)? Go here

PS Carli Adby, of Carli-Art Photography, attended my last seminar and "Really enjoyed your seminar so again, many thanks for the invite as I found it extremely useful..."

- In order to compete with and beat your competitors you need to know and understand them

- Large companies take a very methodical approach to this and may use specialist CI providers

- Lots of different pieces of information are put together to produce a picture of the competitors strengths, weaknesses, performance and intentions

- The principles can be simplified and used by small businesses

Why do you need competitive intelligence?

- To pick up new products and trends in your market

- To identify new markets

- To improve your understanding of what is important to your customers

- To adjust your proposition and positioning to make the most of relative strengths and weaknesses

- To take advantage of opportunities such as competitor failure

How do you gather competitive intelligence?

Online

o Their website

o Social media sites

o Newspapers

o Filings (Companies House)

o Job ads

o Press releases

Offline

o Their marketing materials, brochures, pricelists

o Trade shows

o Suppliers/partners/sub-contractors

o Their customers, your customer surveys

o Trade press

How should you do this in a small business?

- Keep a simple file of information you pick up about your key competitors

- Periodically, plan time to do a few hours research on them

- Periodically, plan time to review your proposition and positioning against this information using Competitor Analysis

- Adjust your proposition and look at the new opportunities suggested

For more business advice for business owners go here

Want to know how much your company is worth (and why)? Go here

PS Carli Adby, of Carli-Art Photography, attended my last seminar and "Really enjoyed your seminar so again, many thanks for the invite as I found it extremely useful..."

Tuesday, 15 June 2010

Product Portfolio Analysis and Small Businesses

What is product portfolio analysis?

- This is a technique developed by the Boston Consulting Group to manage different products within a company's portfolio

- It was designed for large corporates but can be useful for smaller businesses too

It evaluates products or services by their market share against their market growth using the below matrix known as the "Boston Box"

Why are these two factors important?- A growing market means individual suppliers can grow with it without fighting for share and so putting pressure on margins

- A high market share means that prospects think of you first and so your sales cost less and growth is faster

- As a small business if you know your market size, growth and share already then you are probably in a niche and the BCG Box can be applied as shown